AI-enabled Services Part VI: Distribution and Durable advantage

An emerging playbook for AI-native service businesses

Introduction

The idea that AI will transform services is close to consensus now. AI has the potential to invigorate previously sleepy industries, which have long resisted meaningful change, even as SaaS tools flooded the landscape.

But in many such markets, the winning path isn’t to sell more AI software. It’s to go full-stack and operate as an AI-native service provider.

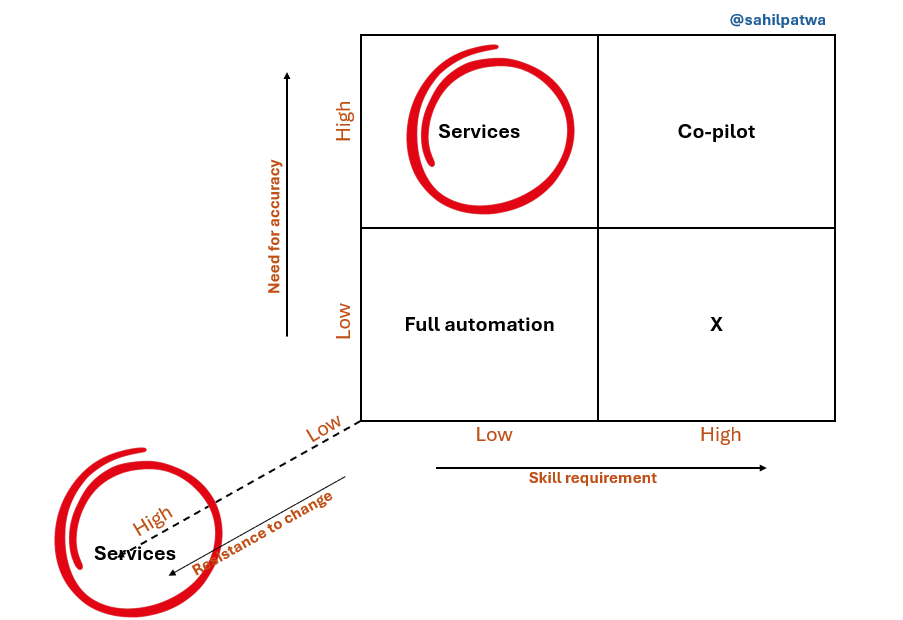

I quite like this 2x2 (I’ve recreated a cleaner version below) to visualize where AI-native services make sense, but I’d tweak it slightly. I would add a third axis around willingness to change in industries where both supply (service providers) and demand (end-customers) resist AI adoption, AI-native services have a distinct edge. I’ve seen multiple AI-enabled or agentic software companies stall around the $5–8M ARR mark — not due to product issues, but due to this type of market inertia.

In this piece, I break down two key questions for founders building in this space:

How to win distribution

How to build sustained advantage

A. How to win distribution?

While AI-native service companies have a strong technological advantage in delivering the service, incumbent service providers have the advantage of already owning customer relationships. In order to create a successful (scalable, fast-growing, profitable) AI-enabled services business, founders will need to be very thoughtful about how to build distribution. I see four different levers for this:

1. Turbocharge GTM with AI

In transactional spaces where contracts aren’t deeply recurring, AI can power GTM by ensuring you're (a) the fastest to respond, and (b) the one delivering the best quality response.

While AI SDRs are transforming SaaS sales, many traditional service providers — say insurance brokers — have never heard of 11x or Landbase. They certainly wouldn’t know how to build a voice-based lead qualifier using ElevenLabs. That’s a real edge for AI-native GTM teams.

Of course, this edge won’t last forever (AI-native competitors will adopt the playbook, incumbents will reluctantly adopt vertical-specific GTM tools) - but still, there’s probably at least a 12–18 month window where AI-powered GTM can reign free.

2. nX superior offering

The obvious way for AI-enabled service businesses to win customers is through a better offering compared to incumbents - not incrementally better, but at least 2-3x better - sufficient to convince someone to switch providers. This could take many forms, but will roughly be on one/more of these dimensions:

Volume (do more)

Speed (do faster)

Cost (do cheaper)

Accuracy (do measurably better)

The true differentiator comes when AI-native companies can unlock something which wasn’t possible before. For instance, AI may allow you to analyze 100% of receipts instead of sampling 10%, or deliver same-day quotes instead of waiting five business days. Tegus is a great example. They used AI to unlock something no expert network had offered before — not just access to individual experts, but also the ability to leverage a rich library of past interview transcripts across customers. This turned previously siloed insights into a searchable, reusable knowledge base.

3. Ride a demand-supply gap tailwind

Industries where there has been a sudden surge in demand (typically caused by some big macro/regulatory dislocation) are great opportunity-spaces for this GTM play. Existing suppliers are unable to catch up to this demand peak, and this creates an “easy mode” entry point for AI-native players.

A case in point: Accounting and Tax Advisory in the UAE. This is the first year for mandatory VAT filings, and tens of thousands of businesses are scrambling to find service providers.

4. Acquire distribution inorganically

We have written about this motion (dubbed AI-powered Roll-ups) extensively — you can read about it here (parts I, II, III, IV, V) and check out this public database of companies already scaling through Roll-ups.

B. How to create a sustained advantage

While solid GTM could help win initial distribution, sustained value creation would need something more - a strategic advantage that the business accumulates over time. From my vantage point, I see 5 potential sources of advantage:

1. Network Effects

The OG (and my favourite) - very hard to build, but even harder to dismantle. Several categories of service businesses benefit greatly from network effects (e.g. 2-sided marketplaces like recruiting/staffing, expert networks, sell-side IB). AI-native companies could leverage technology to outperform (in volume/speed/quality) the incumbents and get the nfx flywheel to start spinning

2. Reputation/ Marquee Logos

In several industries, like advisory services, who your customers are often matter a lot more than how many they are, or how much revenue they give you. In such industries, acquiring logos of marquee customers early on is going to be vital. Companies that have the right logos, might win against even scaled businesses that don’t. This is where publicly positioning yourself as an AI-native player might help you capitalize on the boardroom AI hype and get your foot into the door.

3. Access to Human Capital Networks

AI may reduce headcount, but it also raises the bar for remaining humans-in-the-loop. Companies that have an unfair access to the right AI-fluent talent pool will be able to build enduring value in this space. This is especially true for industries where service providers need to be certified and hence the overall pool of candidates is finite and difficult to expand.

This is a big one. AI-native services firms will look very different from traditional services organizations — new org structures, new mindsets, new cultures. Being able to create a space where AI-fluent talent wants to work will be a “trade secret” hiding in plain sight.

4. Proprietary Workflows/ Process Design IP

This is the "Operational Excellence" play on steroids. AI-native services are essentially a complex interplay of platforms, processes and people. Great execution here requires thousands of small design decisions that collectively result in superior service. The resulting workflows could not only provide organizations with the ability to outperform competitors on service delivery, but they’re also difficult to reverse engineer, because unlike software not all parts of the offering are visible externally. Piecemeal copying doesn’t work unless it’s aligned with the rest of the playbook.

Some people are starting to refer to this as “taste” (see also).

5. Data flywheels

The notion of a data flywheel — where more data improves the product and attracts more users, creating even more data — is seductive, and valid.

But in practice, it’s often hard. More data only helps if it’s the right data, used the right way. In agentic applications, you’re not building foundational models; you’re using those foundational models to essentially build workflows. Sure, more data does help finetune the models where relevant, but the reality is that you often need orders of magnitude more data to get a meaningful delta in output (I see finetuning output as a log function on input data).

That said, RLHF data and good old A/B testing results still matter. They help shape the “taste” of your system.

Conclusion

Having a deep understanding of the industry dynamics, and the resultant strategic imperatives early on, is going to be vital to enduring success for founders (and enduring alpha for investors).

Those who misread the terrain risk chasing the wrong levers.

For instance, focusing on growing revenue through sub-scale customers may backfire in markets where marquee logos matter more. Or, overindexing on scale & margins early on might come at the expense of internal culture and might distort access to human capital. Similarly for investors, investing based on scale of revenues might be a poor indicator of success if “taste” is what would drive long-term value creation.

It's also worth noting that barring data flywheels, most of these advantages resemble traditional services moats. That’s a healthy reminder: at the end of the day, we are still building services businesses.

As the AI-native services playbook is still being written, I am excited to discover more avenues for building strategic advantage, and more GTM hacks. I’m closely following this space and genuinely excited about what’s to come. If you're building an AI-native services business, I’d love to exchange ideas. Feel free to reach out via Twitter, LinkedIn, or email.